Intro

In this article I want to focus on the concept of selling on time and not on price. A lot of advisors and their clients focus extremely hard on the initial price of the product and to tell you the truth I understand why. We all want value. We also want to know that when we pay more for a product or service that we get more from it. People always want to stretch every dollar to save more of their money for the fun stuff and let's face it life insurance is seriously important but it does not fall into the category of the fun stuff.

Now price is extremely important, and so is value. I'm sure anyone in a sales role has heard and even maybe even recited that "Price only matters in the absence of value. That's true but even when selling on value price is still an important factor, particularly when there are multiple options all with different prices and different values.

To make communicating value and price of multiple products even more challenging your customers are conditioned to compare products and do their own research before they purchase, some of our favourite retailers make it the default way to shop (*cough* Amazon *cough*). As the popularity of "marketplace" shopping (like Amazon) increases, so too will the customers need for transparency and simplicity. This ease of transaction becomes the goal post for all other goods and services the customer uses and is paramount to a successful sales experience.

Seeling Around Time instead of Price

Ok if the price is so important why did I call this article selling on time and not price, well what I mean is let's not make the price the first priority. We know the price is always going to be an important factor but let's start with one critical question that is going to set up our whole presentation. I want you to think about asking this question to a prospect before presenting your LDA report and it's a critical question that is going to help you sell more of the right product to your clients and increase your revenue.

The questions is very simple

When do you want your insurance to end?

Wait, as long as it takes...

The answer you are looking for is when I die, or when I retire, or when the house is paid off. Goals are different at different stages of life but by asking when do you want your insurance to end we have now established a time frame to work off.

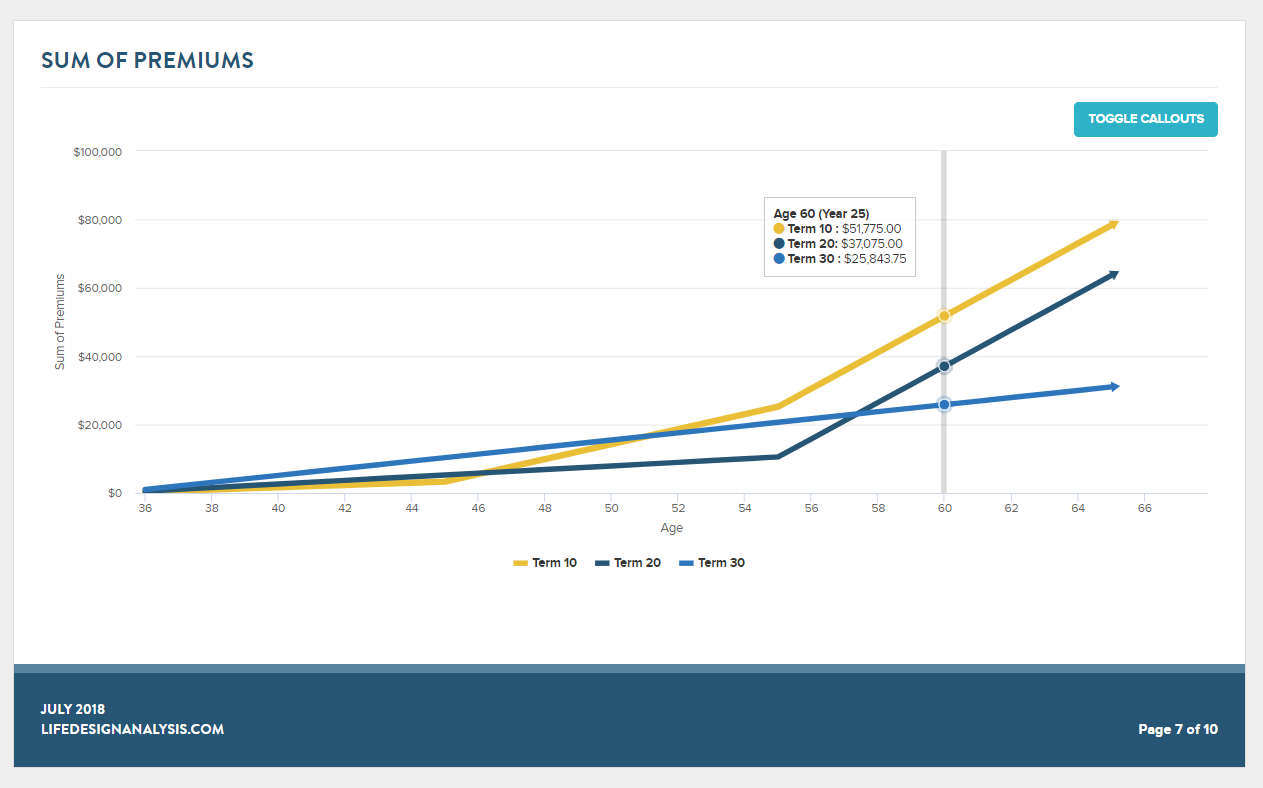

Its not often people have a need for Life Insurance for just 1 or two years it's more to likely they will have a need for 30-60+ years depending on their age, however by asking the simple question of When do you want your insurance to end? we have them establish a timeframe that we can help position multiple suitable acceptable options (MESO) for our clients at different price points. This also creates an opportunity to leverage Asymmetrical Dominance. This strategy works because it quickly and easily shows clients the long-term view of how different products operate over the timeframe that they helped establish. It also generally shows that longer-length products are generally the more affordable option over the course a person will need insurance. Let me show you what I mean with a few case studies.

Young Couple with New Kids/House

This client has cash flow concerns with lots of new liabilities and challenges, in any case, I would suggest a presentation that illustrates differnt term lengths, all the way to the total length of time they plan to hold the Mortgage. This T10 vs T20 vs T30 presentation is perfect to show them thier options in a clear way. In the report I have also added a Life Insurance 101 concept page,they may be new to life insurnace and benefit from a high level overview of the types of insurance. Think about customizing your own report note if you work in a market niche.

If cash flow is really an issue illustrate a Term Ten Exchanged at the 5th year or a Layered Strategy designed around the pay down of their mortgage.

Focused on Retirement

This is the person who is only wanting insurance till they retire. Often the assumption is they will have no need for insurance after they retire as they will have either saved enough or they will have paid off liabilities. For this client, I would illustrate these options that highlight different price points but clearly show the limitations if retirement is not exactly on schedule.

With LDA you can illustrate nearly any insurance situation with any kind of product on the market, Sign up Free and we will show you how! No credit card on sign Up and full support!

When I die

This person has a permanent need for insurance, this could be to fund a liability at a lower cost (think to pass on a cottage to kids) or a corporate client who wants to move money from the balance sheet to something more tax efficient on withdrawal. Think of this kind of presentation comparing different permanent insurance options at different price points. Customize your presentation in LDA with whatever products you would like to illustrate, brand the report with your logo, even toggle between different dividends and plan assumptions live!

It changes

This is actually a pretty common and a strategy that fits a lot of clients and probably does not get shown enough. I would show a layered Strategy like this.

A layered strategy shows clients they can reduce their coverage as their needs change and their liabilities decrease (kids graduate, the house is paid off). It's a great way to illustrate to your clients that they can still have the right insurance for their needs at the right time and it does not have to cost an arm and a leg. Add a custom note to explain why the coverage is dropping or a note that they could re-apply or convert should they so choose.

Conclusion

While price is going to be a huge driver in the sale of any product by framing the cost of life insurance over the proper length of time the person needs Life Insurance (or Critical Illness) is going to result in a more suitable product for your client, increased sales and better retention as a result of properly educated clients. Want to put this method to the test Sign Up for our Free Trial or book a training session with Jon or Nik from our support staff to see how Life Design Analysis can help your practice.